Spending days engaging clients? Chasing late payments? Dealing with scope creep? We get it. Ignition helps accounting and professional services businesses reclaim time, profitability and cash flow. Automate proposals, billing, payments and workflows in a single platform.

Transform the way your firm engages clients, bills and gets paid for all client work. It's time to start maximizing your revenue, cash flow and efficiency with Ignition.

Digital proposals

Start client relationships on the right foot with time-saving proposals clients can review and sign online within minutes.

Engagement letters

Gain clarity with automated client engagement letters that ensure you're always compensated for your work.

Automatic payments

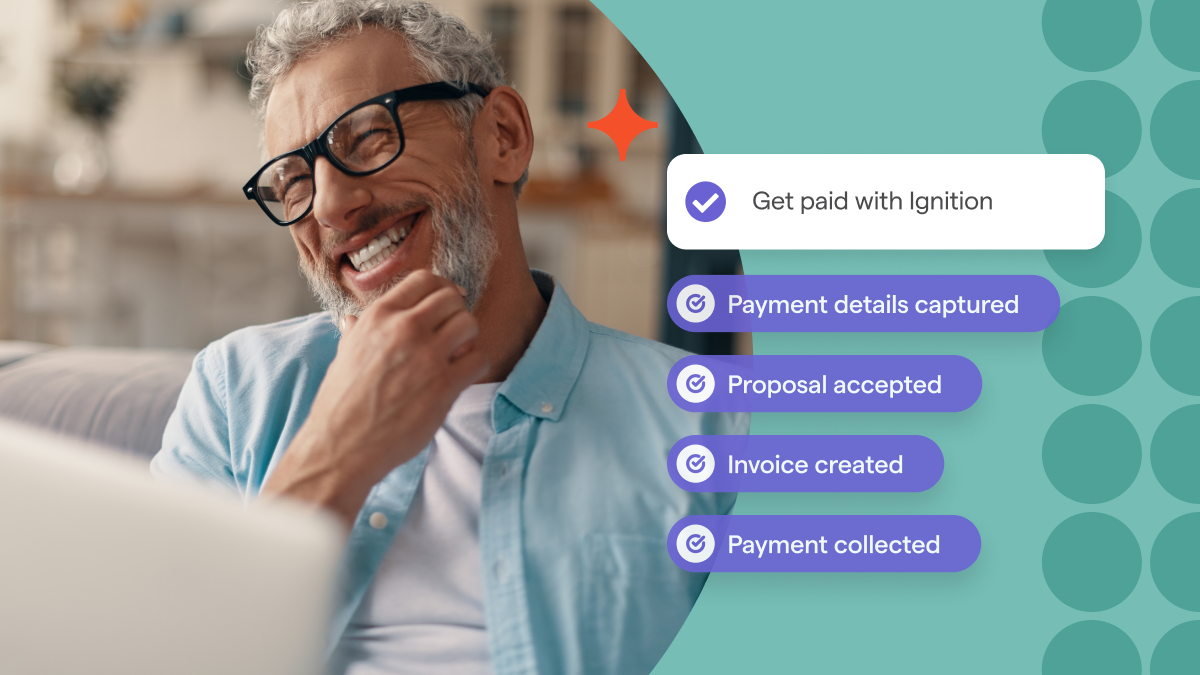

No more chasing clients. Make payments automatic when proposals are signed and no one has to worry about paying or getting paid again.

Automated billing

Set it and forget it. Let client invoices and payments happen in the background and save time to focus on actual work.

Automated workflows

Run your business on autopilot. Connect your favorite apps to Ignition and automated workflows will swing into action the moment your proposal is signed.

Business dashboards

Make faster, more confident decisions with clear visibility into your sales pipeline, upcoming client renewals, and the ability to forecast revenue in one place.

Stop doing work for free. Start engaging clients with a clear scope of work, pricing and terms from day one with branded online proposals and engagement letters. When the scope changes, simply adjust your services or bill instantly for ad hoc work. Just like Logan Graf (Owner) at The Graf Tax Co.

Stop wasting precious time on admin. Start saving countless hours with templated proposals that are quick to create and send, and easy for clients to sign. Then simply set and forget as automated workflows swing into action to take care of invoicing and payment collection. Just like Enae Jackson-Atkins (Owner) at Esquire Accounting.

Stop chasing clients for late payments. Start capturing payment details upfront in proposals and automating fee collection. When you connect Ignition to QuickBooks Online or Xero, you’ll put invoicing and reconciliation on auto-pilot. Just like Marie Greene (Founder) at Connected Accounting.

Stop doing work for free. Start engaging clients with a clear scope of work, pricing and terms from day one with branded online proposals and engagement letters. When the scope changes, simply adjust your services or bill instantly for ad hoc work. Just like Karla Hourigan (Co-founder) at MAD Wealth.

Stop wasting precious time on admin. Start saving countless hours with templated proposals that are quick to create and send, and easy for clients to sign. Then simply set and forget as automated workflows swing into action to take care of invoicing and payment collection. Just like Andrew Van De Beek (Founder) at Illumin8.

Stop chasing clients for late payments. Start capturing payment details upfront in proposals and automating fee collection. When you connect Ignition to QuickBooks Online or Xero, you’ll put invoicing and reconciliation on auto-pilot. Just like Sharon McClafferty (Director) at Slipstream Coaching.

Start every client relationship on the right foot with time saving, digital proposals that are quick to prepare, easy to sign, and make the right first impression.

Scope creep is real. Fortunately, Ignition helps everyone stay clear on engagement terms, so you can feel confident in your client relationship, and get paid for all your work.

Don't stress over chasing clients and late payments. Collect payment details upfront, and make paying and getting paid something no one has to worry about ever again.

Gain visibility and become more profitable with a single source of truth that puts you in control, helping you review performance, forecast revenue, and plan ahead.

Set it and forget it. Let client invoices and payments happen in the background and save time to focus on actual work. Enjoy greater efficiency and control with client billing all in one place.

Save hours on admin by connecting Ignition to your business apps. Automate invoicing and mundane workflows from the moment your client signs the proposal.

Join the 7,000+ accounting and professional services businesses that have transformed how they do business with a 14 day free trial. No credit card needed.

Unfortunately, Ignition doesn't support payments in South Africa, but it's something we're working on in the future.

You'll still be able to engage clients seamlessly with online proposals and automated engagement letters, and run your business on autopilot by connecting apps to Ignition.